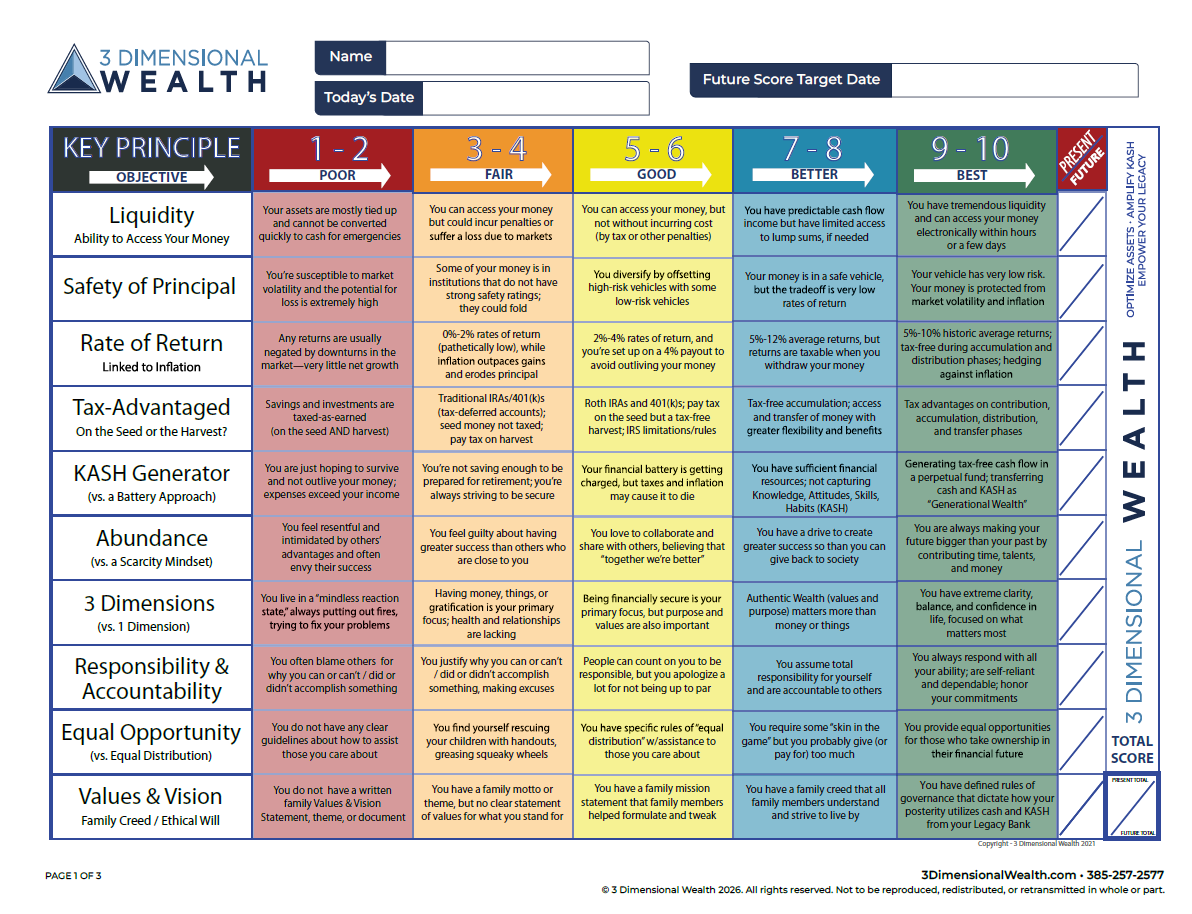

STEP 2: Score Yourself

Enter your name, today’s date, and a target date for your future score goal. Then score yourself in each row/category by dragging the sliders to rank your present progress and future score goal. When done, hit "Next" to review your entries.|

KEY PRINCIPLE

OBJECTIVE

|

1 - 2

POOR

|

3 - 4

FAIR

|

5 - 6

GOOD

|

7 - 8

BETTER

|

9 - 10

BEST

|

Present

0

Future

0

|

|---|---|---|---|---|---|---|

|

Liquidity

Ability to Access Your Money

|

Your assets are mostly tied up and cannot be converted quickly to cash for emergencies

|

You can access your money but could incur penalties or suffer a loss due to markets

|

You can access your money, but not without incurring cost (by tax or other penalties)

|

You have predictable cash flow income but have limited access to lump sums, if needed

|

You have tremendous liquidity and can access your money electronically within hours or a few days

|

|

|

1

|

||||||

|

1

|

||||||

|

Safety of Principal

|

You're susceptible to market volatility and the potential for loss is extremely high

|

Some of your money is in institutions that do not have strong safety ratings; they could fold

|

You diversify by offsetting high-risk vehicles with some low-risk vehicles

|

Your money is in a safe vehicle, but the tradeoff is very low rates of return

|

Your vehicle has very low risk. Your money is protected from market volatility and inflation

|

|

|

1

|

||||||

|

1

|

||||||

|

Rate of Return

Linked to Inflation

|

Any returns are usually negated by downturns in the market—very little net growth

|

0%-2% rates of return (pathetically low), while inflation outpaces gains and erodes principal

|

2%-4% rates of return, and you're set up on a 4% payout to avoid outliving your money

|

5%-12% average returns, but returns are taxable when you withdraw your money

|

5%-10% historic average returns; tax-free during accumulation and distribution phases; hedging against inflation

|

|

|

1

|

||||||

|

1

|

||||||

|

Tax-Advantaged

On the Seed or the Harvest?

|

Savings and investments are taxed-as-earned (on the seed AND harvest)

|

Traditional IRAs/401(k)s (tax-deferred accounts); seed money not taxed; pay tax on harvest

|

Roth IRAs and 401(k)s; pay tax on the seed but a tax-free harvest; IRS limitations/rules

|

Tax-free accumulation; access and transfer of money with greater flexibility and benefits

|

Tax advantages on contribution, accumulation, distribution, and transfer phases

|

|

|

1

|

||||||

|

1

|

||||||

|

KASH Generator

(vs. a Battery Approach)

|

You are just hoping to survive and not outlive your money; expenses exceed your income

|

You're not saving enough to be prepared for retirement; you're always striving to be secure

|

Your financial battery is getting charged, but taxes and inflation may cause it to die

|

You have sufficient financial resources; not capturing Knowledge, Attitudes, Skills, Habits (KASH)

|

Generating tax-free cash flow in a perpetual fund; transferring cash and KASH as "Generational Wealth"

|

|

|

1

|

||||||

|

1

|

||||||

|

Abundance

(vs. a Scarcity Mindset)

|

You feel resentful and intimidated by others' advantages and often envy their success

|

You feel guilty about having greater success than others who are close to you

|

You love to collaborate and share with others, believing that "together we're better"

|

You have a drive to create greater success so that you can give back to society

|

You are always making your future bigger than your past by contributing time, talents, and money

|

|

|

1

|

||||||

|

1

|

||||||

|

3 Dimensions

(vs. 1 Dimension)

|

You live in a "mindless reaction state," always putting out fires, trying to fix your problems

|

Having money, things, or gratification is your primary focus; health and relationships are lacking

|

Being financially secure is your primary focus, but purpose and values are also important

|

Authentic Wealth (values and purpose) matters more than money or things

|

You have extreme clarity, balance, and confidence in life, focused on what matters most

|

|

|

1

|

||||||

|

1

|

||||||

|

Responsibility & Accountability

|

You often blame others for why you can or can't / did or didn't accomplish something

|

You justify why you can or can't / did or didn't accomplish something, making excuses

|

People can count on you to be responsible, but you apologize a lot for not being up to par

|

You assume total responsibility for yourself and are accountable to others

|

You always respond with all your ability; are self-reliant and dependable; honor your commitments

|

|

|

1

|

||||||

|

1

|

||||||

|

Equal Opportunity

(vs. Equal Distribution)

|

You do not have any clear guidelines about how to assist those you care about

|

You find yourself rescuing your children with handouts, greasing squeaky wheels

|

You have specific rules of "equal distribution" w/assistance to those you care about

|

You require some "skin in the game" but you probably give (or pay for) too much

|

You provide equal opportunities for those who take ownership in their financial future

|

|

|

1

|

||||||

|

1

|

||||||

|

Values & Vision

Family Creed / Ethical Will

|

You do not have a written family Values & Vision Statement, theme, or document

|

You have a family motto or theme, but no clear statement of values for what you stand for

|

You have a family mission statement that family members helped formulate and tweak

|

You have a family creed that all family members understand and strive to live by

|

You have defined rules of governance that dictate how your posterity utilizes cash and KASH from your Legacy Bank

|

|

|

1

|

||||||

|

1

|

||||||

| TOTAL SCORE: |

Present

0

100

Future

0

100

|

|||||

STEP 3: Review Your Scorecard

Here’s a look at your entries. If it looks right, just click “Next.” If you want to make any changes, click on “Previous” to update your scores. When you’re done, click "Next” to review it one more time, then click "Next" to go to the last step.|

KEY PRINCIPLE

OBJECTIVE

|

1 - 2

POOR

|

3 - 4

FAIR

|

5 - 6

GOOD

|

7 - 8

BETTER

|

9 - 10

BEST

|

Present

0

Future

0

|

|---|---|---|---|---|---|---|

|

Liquidity

Ability to Access Your Money

|

Your assets are mostly tied up and cannot be converted quickly to cash for emergencies

|

You can access your money but could incur penalties or suffer a loss due to markets

|

You can access your money, but not without incurring cost (by tax or other penalties)

|

You have predictable cash flow income but have limited access to lump sums, if needed

|

You have tremendous liquidity and can access your money electronically within hours or a few days

|

Present

1

Future

1

|

|

Safety of Principal

|

You're susceptible to market volatility and the potential for loss is extremely high

|

Some of your money is in institutions that do not have strong safety ratings; they could fold

|

You diversify by offsetting high-risk vehicles with some low-risk vehicles

|

Your money is in a safe vehicle, but the tradeoff is very low rates of return

|

Your vehicle has very low risk. Your money is protected from market volatility and inflation

|

Present

1

Future

1

|

|

Rate of Return

Linked to Inflation

|

Any returns are usually negated by downturns in the market—very little net growth

|

0%-2% rates of return (pathetically low), while inflation outpaces gains and erodes principal

|

2%-4% rates of return, and you're set up on a 4% payout to avoid outliving your money

|

5%-12% average returns, but returns are taxable when you withdraw your money

|

5%-10% historic average returns; tax-free during accumulation and distribution phases; hedging against inflation

|

Present

1

Future

1

|

|

Tax-Advantaged

On the Seed or the Harvest?

|

Savings and investments are taxed-as-earned (on the seed AND harvest)

|

Traditional IRAs/401(k)s (tax-deferred accounts); seed money not taxed; pay tax on harvest

|

Roth IRAs and 401(k)s; pay tax on the seed but a tax-free harvest; IRS limitations/rules

|

Tax-free accumulation; access and transfer of money with greater flexibility and benefits

|

Tax advantages on contribution, accumulation, distribution, and transfer phases

|

Present

1

Future

1

|

|

KASH Generator

(vs. a Battery Approach)

|

You are just hoping to survive and not outlive your money; expenses exceed your income

|

You're not saving enough to be prepared for retirement; you're always striving to be secure

|

Your financial battery is getting charged, but taxes and inflation may cause it to die

|

You have sufficient financial resources; not capturing Knowledge, Attitudes, Skills, Habits (KASH)

|

Generating tax-free cash flow in a perpetual fund; transferring cash and KASH as "Generational Wealth"

|

Present

1

Future

1

|

|

Abundance

(vs. a Scarcity Mindset)

|

You feel resentful and intimidated by others' advantages and often envy their success

|

You feel guilty about having greater success than others who are close to you

|

You love to collaborate and share with others, believing that "together we're better"

|

You have a drive to create greater success so that you can give back to society

|

You are always making your future bigger than your past by contributing time, talents, and money

|

Present

1

Future

1

|

|

3 Dimensions

(vs. 1 Dimension)

|

You live in a "mindless reaction state," always putting out fires, trying to fix your problems

|

Having money, things, or gratification is your primary focus; health and relationships are lacking

|

Being financially secure is your primary focus, but purpose and values are also important

|

Authentic Wealth (values and purpose) matters more than money or things

|

You have extreme clarity, balance, and confidence in life, focused on what matters most

|

Present

1

Future

1

|

|

Responsibility & Accountability

|

You often blame others for why you can or can't / did or didn't accomplish something

|

You justify why you can or can't / did or didn't accomplish something, making excuses

|

People can count on you to be responsible, but you apologize a lot for not being up to par

|

You assume total responsibility for yourself and are accountable to others

|

You always respond with all your ability; are self-reliant and dependable; honor your commitments

|

Present

1

Future

1

|

|

Equal Opportunity

(vs. Equal Distribution)

|

You do not have any clear guidelines about how to assist those you care about

|

You find yourself rescuing your children with handouts, greasing squeaky wheels

|

You have specific rules of "equal distribution" w/assistance to those you care about

|

You require some "skin in the game" but you probably give (or pay for) too much

|

You provide equal opportunities for those who take ownership in their financial future

|

Present

1

Future

1

|

|

Values & Vision

Family Creed / Ethical Will

|

You do not have a written family Values & Vision Statement, theme, or document

|

You have a family motto or theme, but no clear statement of values for what you stand for

|

You have a family mission statement that family members helped formulate and tweak

|

You have a family creed that all family members understand and strive to live by

|

You have defined rules of governance that dictate how your posterity utilizes cash and KASH from your Legacy Bank

|

Present

1

Future

1

|

| TOTAL SCORE: |

Present

0

100

Future

0

100

|

|||||

Level Up

Area You'd Like to Improve

LEARN MORE

PERSONALIZE IT

TAKE ACTION